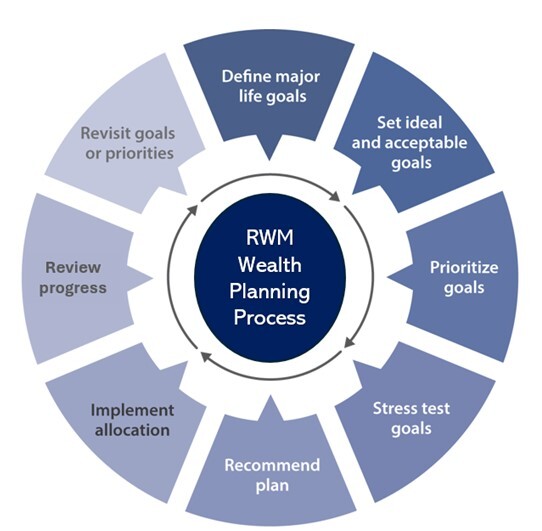

Investment Management Lifecycle

Our eMoney planning process lets us map a realistic financial course designed to help you prioritize and achieve your most important goals through various stages of life.

Based on your objectives, risk tolerance, investment time horizon and current financial situation, we assist you in developing a plan of action and asset allocation that is suitable for your objectives without exposing you to unnecessary risk.

Establish customized benchmarks unique to your plan and objectives to chart your progress toward reaching your goals.

Adjust your plan as necessary to account for life's changes, new opportunities and unexpected events.

CHARTING YOUR PROGRESS

The eMoney Target Zone serves as a foundational tool.

As your goals change, or life events create a need, we use eMoney process to re-evaluate how these changes affect your priorities.

Your eMoney plan will create a benchmark unique to your goals and circumstances as a way to track progress along the way.

IMPORTANT: The projections or other information generated by eMoney® regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. Results may vary with each use and over time. eMoney® methodology: Based on accepted statistical methods, the eMoney tool uses a simulation model to test your Ideal, Acceptable and Recommended Investment Plans. The simulation model uses assumptions about inflation, financial market returns and the relationships among these variables. These assumptions were derived from analysis of historical data. Using Monte Carlo simulation, the eMoney tool simulates 1,000 different potential outcomes over a lifetime of investing varying historical risk, return, and correlation amongst the assets. Some of these scenarios will assume strong financial market returns, similar to the best periods of history for investors. Others will be similar to the worst periods in investing history. Most scenarios will fall somewhere in between. Elements of the eMoney presentations and simulation results are under license from Wealthcare Capital Management LLC. © 2003-2018 Wealthcare Capital Management LLC. All Rights Reserved. Wealthcare Capital Management LLC is a separate entity and is not directly affiliated with Wells Fargo Advisors.

Tax Treatment of Capital Gains and Dividends

How you manage your capital gains and losses and the type of dividends generated by your portfolio can play a major role in determining your after-tax return. To help get the greatest benefit from current tax law, there’s important information you need to understand.

Learn More

Dollar Cost Averaging

Market fluctuations can make it difficult to determine the best time to invest. A widely accepted investment strategy called dollar cost averaging can help smooth out market fluctuations. The key to this long-term strategy is persistence. Whether the market rises or falls, dollar cost averaging can work in your favor.

Learn More

Understanding Wash Sales

When you sell an investment at a loss, the IRS lets you deduct the loss from other capital gains you might have and your taxable income. If you want to continue to be invested in the security, you can purchase the same investment either before or after you sell the original investment.

Qualified Plan Retirement Checklist

When you are a Plan Administrator or a trustee as a named fiduciary for a qualified plan, you must comply with all ERISA rules

Learn More

Saving for College

Giving Children & Grandchildren the Opportunity of a Lifetime

Whether your children or grandchildren are toddlers or teenagers, it’s only a matter of a time before they leave the family home, probably as they head off to college.

Trump Accounts for Children

As part of the One Big Beautiful Bill Act, Congress created a new, custodial-style Traditional Individual Retirement Account (IRA) for children, set to be made available by the Treasure Department on July 4, 2026.

Learn More

2026 Retirement Contributions

As fewer companies offer pensions and Social Security makes up less of the average retiree’s income, you will have to rely more on your own savings for retirement. Making contributions to IRAs and workplace retirement plans (WRP), such as a 401(k), 403(b), SEP IRA, or SIMPLE IRA is an easy way to save for retirement.